In April, I wrote that the proposed pied-à-terre tax deserved careful attention—not emotional headlines. In May, I noted that the proposal was gaining real momentum and that its implications could extend far beyond the luxury market. On May 28, 2026, the measure was enacted as part of New York State's Fiscal Year 2027 budget. Effective July 1, 2026, it imposes an annual surcharge on certain high-value New York City residences that are not the owner's primary residence. The law includes several important exceptions, including residences occupied by qualifying family members and properties leased to tenants under arm's-length leases of at least one year. While the surcharge itself is worthy of attention, the more consequential story may lie elsewhere: how New York City ultimately determines the market value of residential property. That question could have implications extending far beyond pieds-à-terre owners and long beyond the life of this legislation.

How the Tax Works

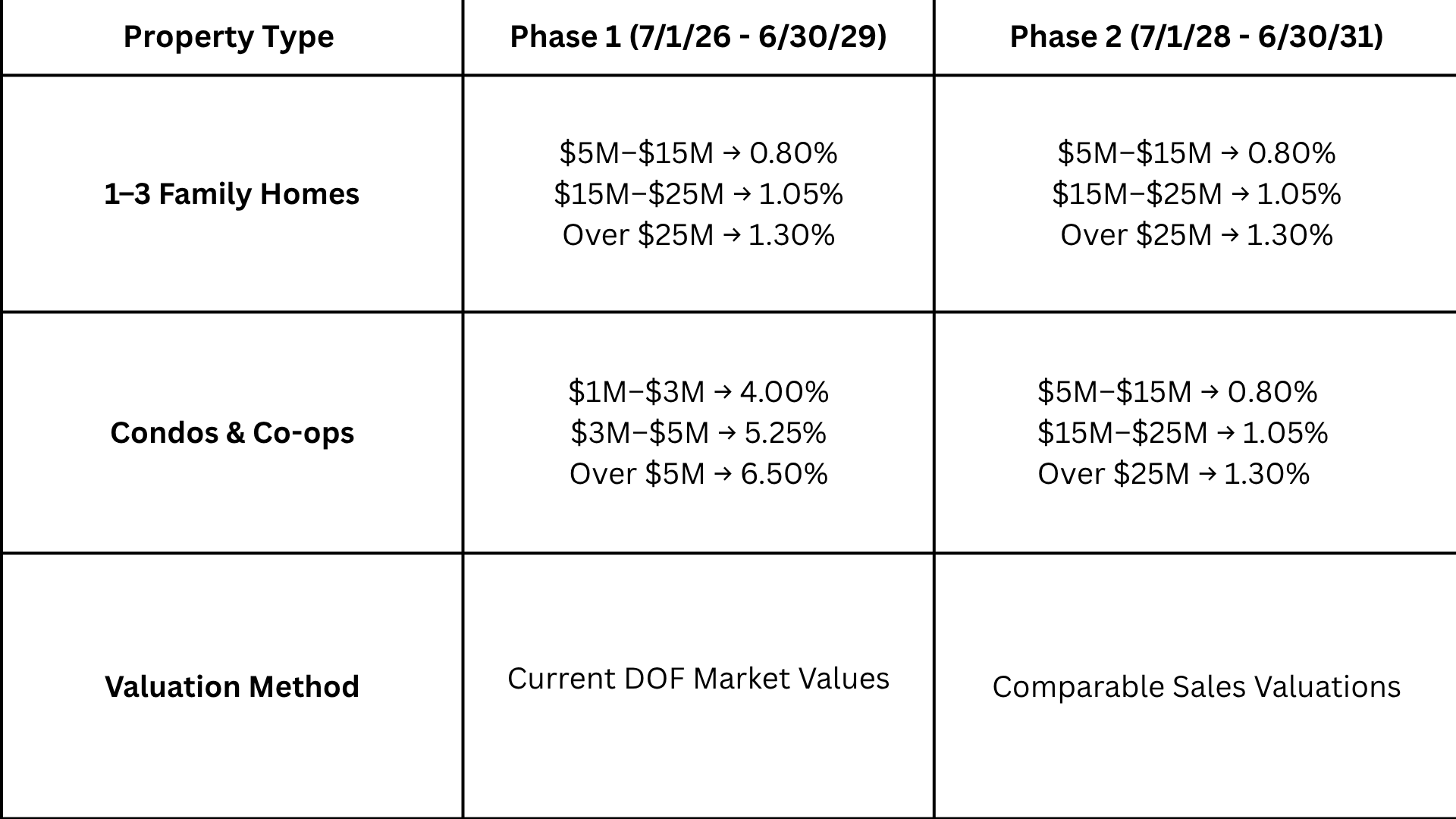

The surcharge will be implemented in two phases over five years as the chart below shows. The two phases differ not only in rates—but in how properties are valued. Phase 1 uses the Department of Finance's existing assessment methodology. Phase 2 shifts to a new mandate: valuations must move closer to actual comparable sales and transaction prices. That distinction is worthy of our concentrated attention.

Why condo/co-op rates are higher in Phase 1: Because DOF currently values co-op and condos well below actual market prices, the surcharge rates are calibrated upward to compensate. Once Phase 2 moves to market based valuations, the rate equalize with single-family homes.

For 1–3 family homes, the rates are identical in both phases, tiered by assessed value: 0.80% ($5M–$15M), 1.05% ($15M–$25M), and 1.30% (over $25M).

For condos and co-ops, the story is strikingly different. In Phase 1, the rates are: 4.00% ($1M–$3M), 5.25% ($3M–$5M), and 6.50% (over $5M). In Phase 2, those rates drop sharply—equalizing with single-family homes at 0.80%, 1.05%, and 1.30% across the same tiers.

That gap is not arbitrary. It is an implicit acknowledgment of something that anyone who works in New York real estate has understood for decades.

The Bigger Question

For more than forty years, New York City's property tax system has operated under a framework established in 1981. State law has required co-ops and condominiums to be assessed not on what buyers actually pay for them, but as though they were income-producing rental buildings—even though co-ops and condos generate no rental income. The result is a valuation system that often bears little resemblance to market reality. Apartments that sell for millions of dollars routinely carry DOF valuations that represent only a fraction of their actual price.

I wrote about this disconnect in 2012—The Conundrum of Rising Real Estate Taxes — describing New York City's property tax structure—"as convoluted as it is complicated, and as political as it is inequitable." Fourteen years later, that observation is the same.

The Phase 1 condo and co-op surcharge rates are set so high precisely because current DOF valuations fall so far below actual selling prices. The legislature needed the rates to compensate for that gap in order to generate meaningful revenue. In many instances, a DOF market value of $1M equates to an actual closing price of $5M or more. Once Phase 2 moves to market-based valuations, the rates equalize.

This is not simply a mechanism for taxing pieds-à-terre. It is the first legislative directive in over four decades to recalibrate how co-ops and condominiums are valued for property tax purposes in New York City. And that has implications for every owner—not only those purchasing a second home.

What to Watch

Many non-primary owners will understandably focus on the amount of their first surcharge bill. But the more consequential concern for any co-op or condo owner in New York City may be what happens when the transition period of Phase 1 ends, and a new Phase 2 valuation methodology is created. Questions are aplenty: How will co-op units—assessed as a share of a building rather than individually—be handled? Is it reasonable to make the co-op board responsible for payment of the tax and then collect reimbursement from the shareholder, as the current law mandates? What happens when a lien is placed on the entire building for non-payment? How will variables like condition and views among other factors that influence market value be processed? Will there be opportunities for the public to review regulations and procedures before a new system takes effect in two years? Attorneys are already anticipating legal challenges, and courts will likely weigh in before 2028 arrives.

If future assessments move substantially closer to actual market prices, the ramifications will extend beyond this five-year annual surcharge—reshaping debates about property tax equity, carrying costs, and the economics of NYC residential real estate for every owner in every price range.

That conversation is worth starting now, not after the methodology is finalized.

As always, I'm happy to talk through what this means for you specifically — whether you're an owner, a buyer, or somewhere in between. Reach out at shirley.hackel@compass.com or 914-980-0371.