February activity followed one of the most active Januarys we’ve seen in a long time. And although it’s the shortest calendar month — further shortened by frigid cold, Presidents’ Day, and two winter storms including a nor’easter bomb cyclone that brought 19.7 inches of snow to Central Park — we are entering the spring housing market with some of the healthiest conditions and most encouraging news we’ve seen in quite a while.

Here are four extremely positive indicators to note as we move forward.

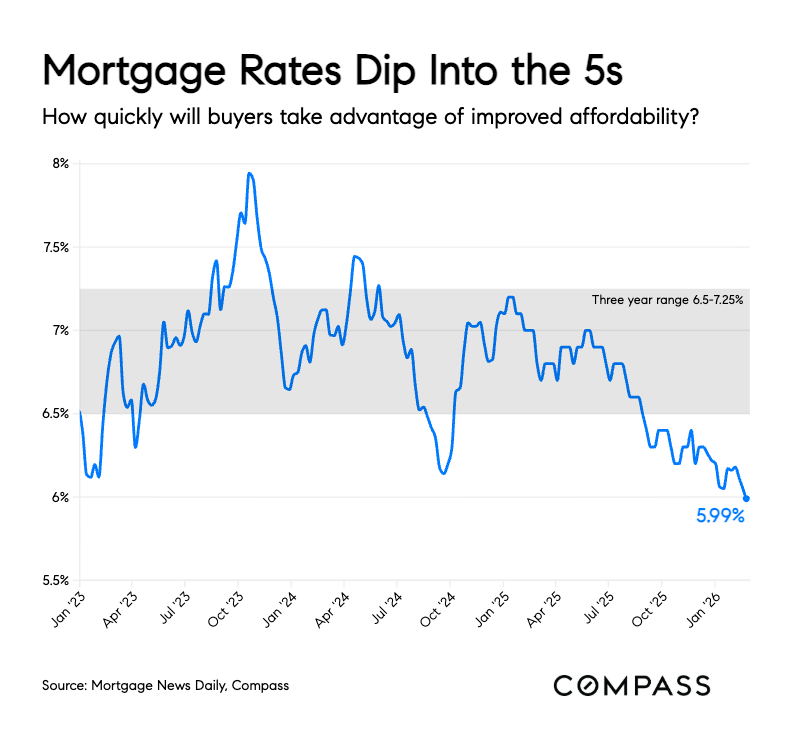

New offerings are coming to market steadily, though quality inventory remains tight. Nationwide, there are about 9% more homes on the market than a year ago, but still 15% fewer than in 2019. Pending sales are up across the board. And — drumroll please — mortgage rates have dipped just below 6% and are now at the lowest level we’ve seen since 2022, approximately 8% lower than they were at this time last year. Entry- and mid-level buyers especially should take note: it may finally be time to exit high-priced rentals. The national average for a 30-year fixed mortgage rate is 5.99%, and refinancing applications are up approximately 130% year-over-year.

NYC rents are surging. Manhattan median rents rose to the third highest level on record, climbing 7.9% to $4,695. Apartment hunters can likely expect record highs this spring. Rental listings declined year-over-year for the seventh time, down 9.3%, while the number of new leases rose a mere 0.5%. The Manhattan vacancy rate was 2.44%, well below the 10-year average.

High end sales continue to make headlines. The Olshan Report, which tracks weekly activity of contracts signed for properties priced at $4M and above, shows that during the banner three-week period from February 2 through February 22, ninety contracts were signed — and 33 of those units, more than one-third, were priced at $10M or higher. Contributing significantly to those numbers were contracts signed at 1122 Madison Avenue, the new development under construction at the southwest corner of 84th Street just one block from Central Park and The Met. Designed by Studio Sofield and developed by Legion Investment Group and Nahla Capital, the condominium began showing from floor plans on January 15th from its sales office at the private Club Colette in the GM Building. As of this writing, 20 of the 26 residences are under contract — nearly 77% of the building — including 18 with asking prices north of $10M. The duplex penthouse, offering 9,350 square feet, a double-height Great Room, and commanding park views, is reportedly in contract at the asking price of $89.5M — the most expensive Upper East Side sale so far this year. There have been four reported price-increase amendments since the filing of the initial Offering Plan .

A new law will impose first-time standards for the timing of co-op board review and approvals. On January 29, 2026 — effective for sales applications submitted as of July 28, 2026 — the New York City Council passed the “co-op timing bill” (Int 1120). Within 15 days of receipt of an application, co-op boards in buildings with 10 or more units must acknowledge receipt or specify what is missing. If no acknowledgment is issued, the application will be deemed complete, and the co-op will then have 45 days to issue a decision, extendable by 14 additional days; any further extension will require the applicant’s consent. Fines will be imposed by the Department of Housing Preservation and Development: $1,000 for a first violation, $1,500 for a second, and $2,000 for third and subsequent violations.

Taken together, these early signals of 2026 suggest a market moving away from hesitation and toward more confidence. Sidelined buyers are re-engaging as financing improves, sellers are coming to terms with more realistic expectations, and rental pressures are motivating decisions to purchase. Well-positioned properties continue to attract meaningful interest, while overpriced offerings are mostly ignored. In short, this is a market that rewards strategy and preparation — not speculation. For those considering a move this year, the coming spring season may offer one of the most balanced opportunities we’ve seen in several cycles.

NEW DEVELOPMENT SPOTLIGHT

Where we feature a noteworthy new development to help buyers weigh co-op versus condo ownership

1122 Madison Avenue

1122 Madison Avenue is especially noteworthy for the way it will blend seamlessly into the fabric of the neighborhood — and for the remarkable speed with which more than 75% of its luxury residences have already sold. The limestone condo tower recalls the days when properties sold from floorplans. Only a few three- and five-bedroom homes remain of the 26 impressive residences—each with private elevator landing, ceiling heights of at least ten feet, and rooms with expansive proportions. Approximately 10,000 square feet of amenity space includes a fitness center by The Wright Fit, squash/basketball court, billiards room, dining room and kitchen, media room, cold plunge pool and spa facilities. Occupancy is slated for Fall 2027. According to the developer, most of the unit buyers, including the penthouse, are New Yorkers. It’s a clear example that today’s buyers increasingly want the architectural gravitas and floor plans of prewar buildings without the hassle of the years-long renovations they often require.

If you’re beginning to think about a move in 2026, and curious how new development compares to resale options, we would be delighted to begin a confidential conversation about opportunities and timing.